OK then.�

But its specific impact on folks won��t work like those yahoos predict. First, what is the yield curve? Second, who cares? And most important,�how and when might it affect you?

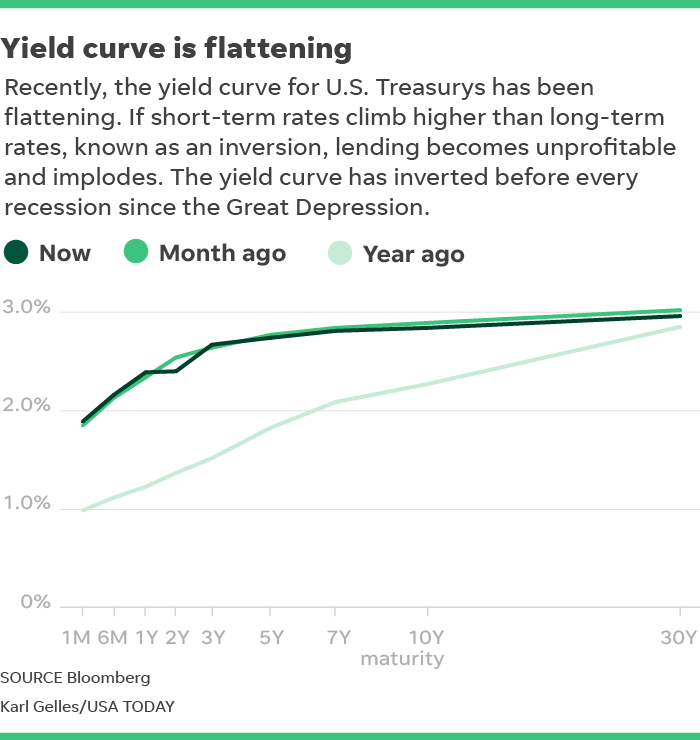

The yield curve is just a line graph showing the interest rate of government bonds at every future maturity (meaning when they come due and repay the principal). So the full curve depicts rates of�bonds from very short term to very long term (from now until 30 years from now). �

The ��line�� uses dates of maturity horizontally from now, moving to the right, through 2048,�and corresponding rates from zero to very high vertically. �

Normally, short rates are lower than longer-term rates. So the line normally slopes gently upward to the right.

.oembed-asset-photo-image { width: 100%; }

Changes in the curve�matter because they affect bank lending, which impacts almost everything, it seems. �

Banks borrow at short-term rates, lend long term�and profit from the difference. So the gap between long and short rates predicts future loan profitability. The bigger the gap, the more eager banks are to lend. The yield curve is a great predictive proxy for future lending. �

Lending matters because loans allow for economically expansive activities. Sally deposits $10,000 at Community Banks-R-Us, which can keep $1,000 in reserve and lend out $9,000 to Jim��s Widgets. Jim uses that to grow his business. Hence lending can fuel growth. So, steeper yield curves spur economic activity. Flatter curves render less.

But when short-term rates exceed long-term rates (commonly called inversion) disaster awaits because lending becomes unprofitable and implodes. The yield curve has inverted before every recession since the Great Depression.�

Headlines warn the yield curve is its flattest in 11 years �� the eve of the global financial crisis. Pundits predict inversion as imminent and a slowdown as definite, or worse.�

They��re wrong in two ways.

First, they��re watching the spread between two-year and 10-year yields. It hardly matters. Banks don��t borrow much at two-year rates. Most funding comes from varied shorter-term deposits.

The valid spreads are 10-year minus overnight (the fed-funds rate) and 10-year minus three-month. They��re both useful. The three-month spread captures more interbank funding and is more sensitive to market forces than the Fed-set rate. But the Conference Board uses the 10-year/fed-funds spread in its Leading Economic Index. It��s the single best leading indicator around (see my July 17, 2017 column). ��

Typically we avoid recession unless both versions invert and remain inverted �� killing lending. They��re also both much wider than that bogus 10-year/two-year spread, which is�just 0.24 percent�but is causing today��s terror.

The 10-year/three-month spread is 0.85 percent. The 10-year/Fed funds spread is 0.92 percent. While these two are flatter than last year, they are very far from inverted.

Tellingly, the yield curves of most of the booming, zooming mid-to-late 1990s were around these levels �� or flatter. Today��s moderate spreads are part of our ��Goldilocks�� economy (see my 5/7/18 column).�

The second error? Almost everyone everywhere misses that the total global yield curve matters much more than America��s. And it��s doing just fine, thank you. Today��s global financial system is super interconnected. Behemoth banks can borrow in low-rate countries such as Germany, transfer funds here, hedge for currency risk and lend to Jim��s Widgets in mere seconds.

The global yield curve combines every developed country��s curve, weighted by the size of each economy. You get Britain��s 0.88 percent�10-year/three-month spread, Canada��s 0.69 percent�gap, Germany��s 0.92 percent, France��s 1.23 percent, Japan��s 0.18 percent�and the rest. Mash them all together based on GDP weighting, and that gets you a 0.9 percent�global spread that��s bouncing along, going nowhere fast. Current U.S. yield curve fears miss this.�

Those headed for the hills will get flattened as our economy keeps steamrolling ahead. I watch the global yield curve�like a hawk, and it will be years before it�inverts, most likely. When it does I��ll warn you. And then bad things will happen.

Until then, don��t get flattened. Expand. Grow. Participate. Start a firm. Own stocks. And enjoy.�

Ken Fisher is the founder and executive chairman of Fisher Investments, author of 11 books, four of which were "New York Times" bestsellers, and is No. 200 on the Forbes 400 list of richest Americans. Follow him on Twitter @KennethLFisher

The views and opinions expressed in this column are the author��s and do not necessarily reflect those of USA TODAY.

�

No comments:

Post a Comment